The Indian Company That Makes What Pratt & Whitney Can’t Fix Fast Enough

How a defect smaller than human hair grounded 835 of the world's newest aircraft, why repairing them takes 300 days instead of 60 and where a precision forging company from Hyderabad fits into the fix

Note: This is for educational purposes only. The views expressed are the author’s own and should not be construed as investment advice.

In my last post on Dynamatic Technologies, I covered the airframe side of the aerospace crisis: 17,000 aircraft in backlog, $11 billion in annual costs to airlines, and how a Bangalore company became Airbus’s trusted supplier of flap track beams and A220 doors after 17 years of flawless execution.

Today I want to cover the other half of the aerospace supply chain. The half that is, right now, causing more financial damage to airlines than the airframe backlog and the production delays combined.

Engines.

Specifically, the Pratt & Whitney Geared Turbofan engine, installed on roughly half the world’s A320neo fleet, the most popular commercial aircraft programme in history. And the catastrophic supply chain failure that has grounded 835 aircraft, stretched MRO shop visits from 60 days to 300 days, triggered an $8 billion recall, and created a scramble for precision-forged engine components that the global manufacturing base was never built to handle at this scale.

Let’s get started!

How a Geared Turbofan Actually Works (And Why It Matters)

Before getting into the crisis, it helps to understand why the GTF engine was such a big deal in the first place, because the same engineering that made it revolutionary also made the recall so painful.

So, a conventional turbofan engine has a fundamental design compromise. The front fan (the large spinning disc you see when you look at a jet engine) is connected by a shaft directly to the low-pressure turbine at the back of the engine. Both therefore, must spin at the same speed. The problem is that each wants to spin at a very different speed. The fan, with its large diameter, works best at about 3,000 to 5,000 RPM. The low-pressure turbine, much smaller in diameter, works most efficiently at 9,000 to 15,000 RPM. Since they share a shaft, engineers compromise: the fan spins a bit faster than ideal (creating noise and inefficiency), and the turbine spins slower than ideal (requiring extra stages to compensate, adding weight and cost).

Pratt & Whitney’s ingenious solution was to put a planetary gearbox between the fan and the turbine. A reduction gear with a ratio of about 3:1. The fan now spins at its optimal 3,200 RPM while the low-pressure turbine spins at its optimal 9,000+ RPM. Each component operates at peak efficiency without constraining the other.

The results were striking. The GTF achieves a bypass ratio of up to 12:1 (meaning 12 parts of air flow around the engine core for every 1 part going through it), compared to about 6:1 for the engine it replaced (CFM56). This translates to 16% lower fuel consumption, 50% noise reduction, and significantly lower emissions. Pratt & Whitney had been developing the concept since the 1990s and spent 20 years in active testing before the PW1100G entered commercial service in 2016.

Airlines chose the GTF because the economics were genuinely compelling. On a narrowbody aircraft flying 3,000+ hours a year, a 16% fuel saving adds up to millions of dollars annually per aircraft. About half the world’s A320neo orders specified the Pratt & Whitney engine rather than the competing CFM LEAP.

Fun Fact: The gearbox worked fine! Pratt & Whitney and industry analysts have repeatedly confirmed that the geared architecture itself, the engineering innovation that made the whole engine possible, has not been the source of problems. The problems, interestingly, came from the engine core, specifically from the materials used to manufacture the highest-stressed components in the hot section!

And that is where the story turns.

The Recall Nobody Saw Coming

In 2020, an in-service IAE V2500 engine (an older Pratt & Whitney design) suffered a blade failure. Investigation revealed that the root cause was contaminated powder metal used in manufacturing critical engine components. The same powder-metal manufacturing process that produced parts for the V2500 was also used for the newer PW1100G Geared Turbofan.

By 2023, Pratt & Whitney had disclosed the full scope: a rare contamination defect in the metal powder used to forge high-pressure turbine discs and compressor discs. These are components that operate at temperatures exceeding 1,000 degrees Celsius while spinning at over 10,000 RPM. Even microscopic impurities in the metal create stress concentration points that, over time, can develop into cracks. If those cracks propagate to a critical length in a disc spinning at that speed, under that heat, the result is what engineers euphemistically call an “uncontained failure.” Fragments of metal exit the engine casing at ballistic velocities.

The scale of the recall: 600 to 700 GTF engines requiring inspection through 2026. RTX Corporation (Pratt & Whitney’s parent) has booked approximately $8 billion in charges. The recall is expected to continue through end-2026 (at the earliest). Some industry participants now believe affected aircraft won’t fully return to service until 2027 or even 2028!!

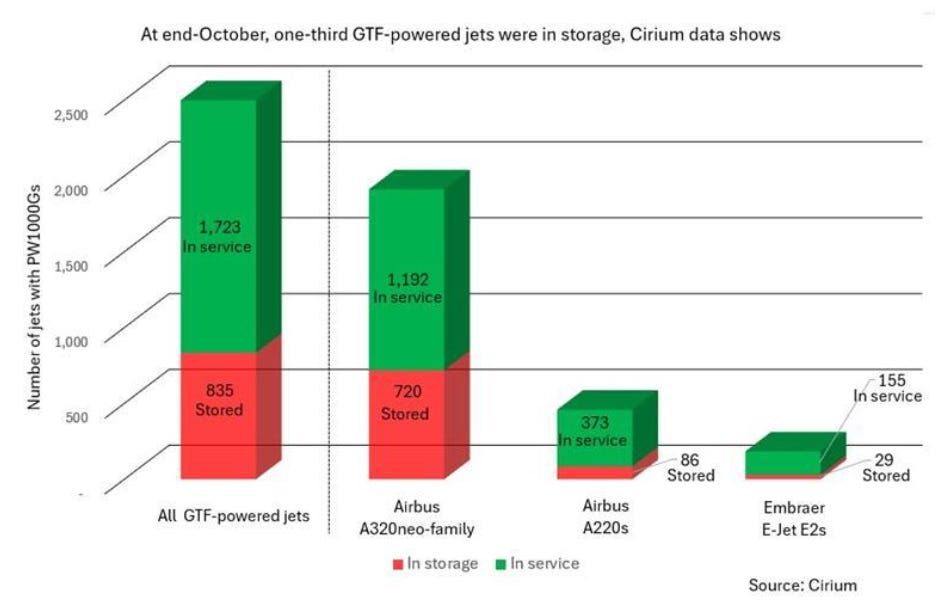

835 Aircraft on the Ground

As of October 2025, according to Cirium fleet data (below) reported by FlightGlobal, 835 aircraft powered by the PW1000G family were in storage globally. That was up from 748 at mid-year, a jump of nearly 90 aircraft in a single quarter. The trend was accelerating, not stabilising.

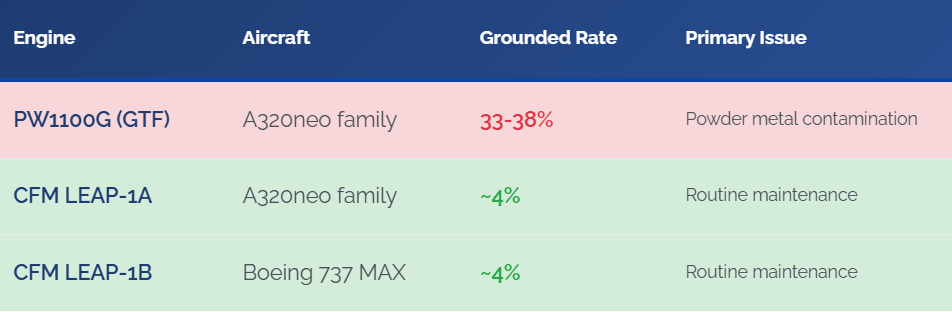

Of these, 720 were A320neo family aircraft out of a global GTF-powered A320neo fleet of 1,912. That is 38% of all GTF-powered A320neos sitting on the ground, unable to carry passengers. For comparison, only about 4% of CFM LEAP-powered narrowbodies are grounded for engine-related issues. One in three vs one in twenty-five.

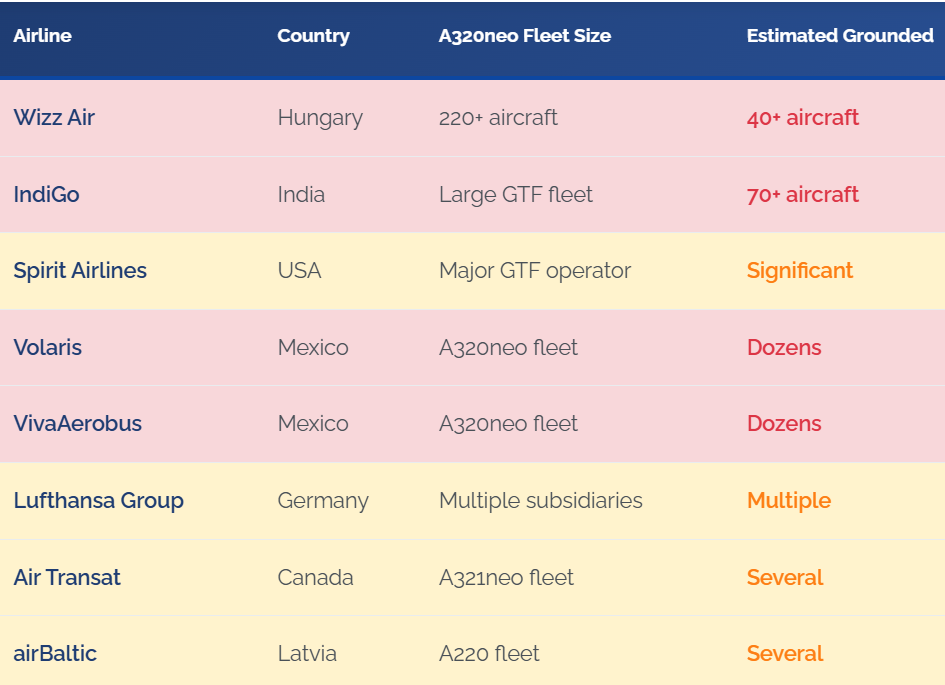

The airline-level impact is severe and spread across every continent! Spirit Airlines has 39 A320neos grounded out of a fleet of 91. Wizz Air, one of Europe’s largest ultra-low-cost carriers, operates with 35 to 41 aircraft grounded at any given time. ITA Airways (Lufthansa’s subsidiary) is seeking approximately €150 million in damages from Pratt & Whitney after having several aircraft parked in Naples for over a year. Swiss International Air Lines is grounding its entire sub-fleet of nine A220-100s in 2026 to conserve scarce engine parts. Latvia’s AirBaltic has dampened its growth plans and resorted to leasing older aircraft to fill the gap.

Closer to home, IndiGo, India’s largest airline and the world’s largest operator of the A320neo family, has had roughly 70 aircraft grounded at various points due to the GTF issue. For context, that is more aircraft than most Indian airlines have in their entire fleet. IndiGo’s CFO Gaurav Negi acknowledged the airline was leasing additional aircraft to sustain operations, while the DGCA approved wet-leases of older A320ceos powered by different engines to keep routes running.

IndiGo reportedly extended leases on older, less fuel-efficient aircraft and scouted the market for available planes powered by anything other than the PW1100G. For Indian passengers, the consequence was tangible: reduced capacity on a network that was growing at double digits, leading to elevated fares on domestic routes through much of 2024 and 2025. When your largest airline has more planes on the ground than GoFirst had in its entire fleet at the time of its shutdown, you know the problem has come home.

And here is where the crisis crosses from operational disruption into something structurally bizarre. Nearly-new A321neo aircraft, planes with less than a decade of service, are being stripped and scrapped for their engines. The second-hand value of a single working PW1100G engine now exceeds the lease value of the airframe it sits on. Airlines and lessors are cannibalising almost-new aircraft because getting a replacement engine from Pratt & Whitney means joining a queue that stretches years into the future. Again, conditions have a way of reshaping economics.

David Chaimovitz, an aerospace aftermarket analyst, told AviTrader in November 2025: “34% of the A320neo GTF fleet is currently parked, and shop visits are still taking 300 days. The issues have not been alleviated.”

Peter Foster, CEO of Air Astana, was blunter on the airline’s Q3 2025 earnings call: “We took the first Neo in October 2016. Here we are now in October 2025, that is nine years, and we are looking at at least another two, if not three more years. We are talking about a 12-year problem minimum.” He went further: “If you look at the litany of problems that this engine has presented to us, I would not call it a short-term problem. What you would have to call it is a significant overall design problem, because evidently, if you have had so many issues with one engine, that demonstrates a lack of robustness of the original design.”

Whether Foster is right about the design (Pratt & Whitney and most independent analysts attribute the problems to manufacturing process contamination, not the geared architecture) is debatable. What is not debatable is the financial impact. Air Astana reported that 14 unplanned GTF engine removals during Q3 2025 alone cost the airline $23.7 million in EBITDA. All 13 of its low-cost subsidiary FlyArystan’s A320neos are parked. The airline is operating with leased older-generation aircraft to fill the gap.

Why 300 Days Instead of 60

A GTF engine MRO (Maintenance, Repair, and Overhaul) shop visit that used to take about 60 days now takes 300 days on average. Understanding why gets to the heart of the supply chain bottleneck, and explains why a company in Hyderabad becomes relevant to this story.

When a GTF engine comes in for inspection under the recall, the high-pressure turbine discs, compressor discs, blades, nozzles, and seals must be removed, inspected (often using advanced non-destructive testing that can detect cracks smaller than a human hair), and in many cases replaced with newly manufactured components made from uncontaminated powder metal.

These replacement components are among the most difficult things to manufacture in all of industrial production. High-pressure turbine blades operate at temperatures exceeding 1,000 degrees Celsius while withstanding centrifugal forces that would tear apart most metals. They are made from nickel-based superalloys, materials like Inconel 718 and René 88DT, engineered to maintain structural integrity under conditions where ordinary metals would literally melt. Manufacturing a single turbine blade involves: powder metallurgy (consolidating metal powder under extreme heat and pressure), precision forging (shaping the superalloy billet on isothermal presses under controlled temperature), multi-axis CNC machining (5-axis work with tolerances of ±0.01mm), heat treatment, surface coating, and multiple stages of non-destructive inspection (ultrasonic, fluorescent penetrant, eddy current).

An isothermal forging press capable of this work costs hundreds of millions of dollars. There are a limited number of them worldwide. Pratt & Whitney announced a new isothermal forging press at its Columbus, Georgia facility that will increase critical component output by 30%. It won’t come online until 2028.

So the 300-day shop visit isn’t because mechanics are slow. It’s because the replacement turbine blades, nozzles, and disc components are physically constrained by the number of qualified manufacturers, the throughput of superalloy processing, and the certification requirements that cannot be shortened. RTX says it has increased maintenance capacity by 35% year-on-year. GE Aerospace has committed $1 billion in 2025 alone to support engine component suppliers. Safran reported aftermarket services revenue growth of 30% in US dollar terms for 2025. The entire global aero-engine MRO supply chain is straining under the combined weight of the GTF recall and normal maintenance on a growing fleet.

The IATA/Oliver Wyman study I cited in the Dynamatic analysis estimated $2.6 billion in excess engine leasing costs for airlines in 2025 alone, as carriers lease engines to keep aircraft flying while their own engines sit in MRO queues.

The bottleneck, to be precise, sits in the hot section of the engine: the turbine blades, nozzle guide vanes, combustor liners, and disc components that operate in the most extreme thermal and mechanical environment of any manufactured product on Earth. The world needs more qualified manufacturers who can forge, machine, and certify these components to aerospace standards. The existing Western supply base (Precision Castparts, Howmet Aerospace, Safran, MTU Aero Engines) is running at or near capacity.

The Blade Maker from Hyderabad

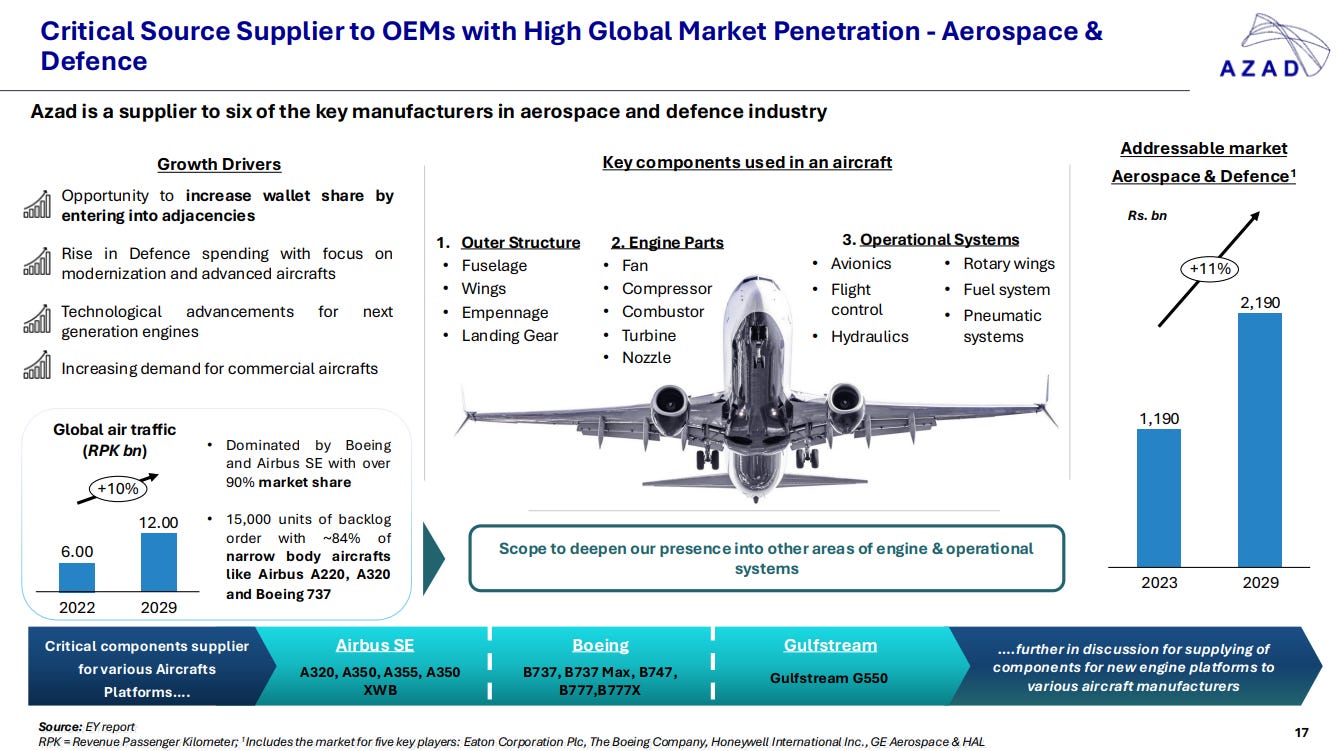

There is a company in Hyderabad that makes turbine blades. Every type of radial and axial flow blade. For gas turbines and for jet engines. For GE, for Siemens Energy, for Mitsubishi Heavy Industries, for Rolls-Royce, for Pratt & Whitney, and for Safran.

That sentence is worth reading carefully, because very few companies on Earth supply hot-section components to all of the world’s major turbine OEMs simultaneously. The qualification process for each OEM takes years, sometimes decade+. The zero-defects requirement is non-negotiable. A single flawed turbine blade in a jet engine spinning at 10,000 RPM at 1,000°C can bring down an aircraft.

The company is Azad Engineering, and it has been doing this since 2008 with a track record of 3.09 million units delivered at literally zero parts-per-million defects.

An Indian Defence Research Wing article from November 2025 described Azad as “a critical supplier of high-precision hot-section components (turbine blades, nozzles, and combustor liners) for GE, Pratt & Whitney, Rolls-Royce, and Safran.” Those are the exact components inside the engine hot section that the GTF contamination crisis is about. The blades that need replacing. The nozzles that need inspecting. The combustor liners that must meet zero-defect standards.

Hyderabad, 1983

Rakesh Chopdar founded Azad Engineering in 1983. The core business in precision engineering began in 2008, and for most of the company’s commercial life, the primary market was energy turbines, not aircraft engines. Azad built its reputation making turbine blades and other hot-section components for the power generation industry: the gas turbines made by GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Baker Hughes, and BHEL that produce electricity in power plants around the world.

This matters for two reasons. First, the metallurgy, the forging, the machining, and the quality requirements for a gas turbine blade operating at 1,200°C in a power plant are essentially identical to those for a jet engine blade operating at 1,000°C at 35,000 feet. The superalloys are the same. The forging processes are the same. The CNC machining tolerances are the same. The non-destructive inspection methods are the same. A company that can make blades for a GE HA gas turbine (the world’s most efficient power generation turbine) has the foundational capability to make blades for a GE GEnx jet engine. The physics don’t materially change because the turbine is bolted to a wing instead of a concrete pad.

Second, the energy turbine business gave Azad something that no amount of capital can buy quickly: decades of documented, audited, zero-defect manufacturing history with the same OEMs that make jet engines. GE’s power division and GE’s aviation division share quality standards. Siemens Energy’s gas turbine quality requirements overlap with aerospace. When Rolls-Royce needed a partner to manufacture complex components for its defence aero-engines, it didn’t go looking for a startup. It went to a company that had already proven, over years, that it could forge and machine superalloy components at zero PPM defects.

The Rolls-Royce contract, announced in January 2024, is a seven-year agreement for Azad to manufacture and supply complex rotating components for defence aircraft engines. Alex Zino, Rolls-Royce’s Executive Vice President of Business Development, said: “As we work towards strengthening the defence ecosystem, we are happy to expand our supply chain in India in partnership with Azad Engineering. The sourcing of complex components from India for aero engine programmes further advances the goal of capability creation in the country.”

In November 2025, Azad signed a Master Terms Agreement with Pratt & Whitney Canada Corporation for the development and manufacture of critical aircraft rotating engine components for strategic engine platforms. The same month, the company confirmed it had signed its first long-term agreement with Safran Aircraft Engines.

Count the OEM relationships. GE (energy and aviation). Siemens Energy. Mitsubishi Heavy Industries. Baker Hughes. Rolls-Royce (seven-year defence engine contract). Pratt & Whitney Canada (long-term agreement for rotating engine components). Safran Aircraft Engines (first long-term agreement). Honeywell. Eaton Aerospace. That is a client list that took 15+ years to build and cannot be replicated by a new entrant in any reasonable timeframe, irrespective of the amount of capital they bring in.

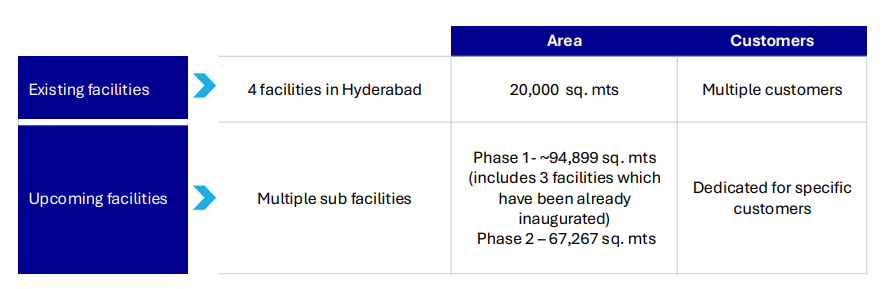

Azad’s Hyderabad facility houses an in-house forge shop, heat treatment unit, advanced 5-axis CNC machining systems, specialised inspection labs, and proprietary manufacturing software. The company produces every type of radial and axial flow blade. It holds NADCAP accreditation (the global aerospace special process quality standard). Between FY2009 and FY2023, it manufactured and delivered 3.09 million precision components.

The Numbers

Q3 FY26 (quarter ending December 2025) was Azad’s strongest quarter ever. Revenue grew 31.4% year-on-year to c.Rs 156 crore. EBITDA surged 40.7% YoY to Rs 60 crore at a margin of 38.6% (up from 35.0% a year ago). PAT grew 40% YoY to approximately Rs 34 crore.

For the nine months ending December 2025, revenue was Rs 433 crore (up 31.8% YoY). The company surpassed its full-year FY25 EBITDA and PAT within just nine months of FY26. Management is guiding 25 to 30% revenue growth and 33 to 35% EBITDA margins on a sustained basis.

The segment split tells the story of where this company is heading. Energy and Oil & Gas contributed about 81% of Q3 revenue (Rs 127 crore), growing 33.5% YoY. Aerospace and Defence contributed about 17% (Rs 26.4 crore), growing 33% YoY. The CEO, Rakesh Chopdar, has said he expects aerospace and defence to eventually contribute to revenues on par with the energy segment. That would imply a roughly 5 to 6x increase from current A&D levels. Account for the existing high growth in O&G segment, and that should tell you management’s view on how they expect Aerospace to perform in terms of growth.

The order book is where the forward visibility sits. As of Q3 FY26, Azad’s total order book stood at approximately Rs 6,500 crore. That is about 14.2 times the company’s full-year FY25 revenue. Among the notable recent contracts: a Phase 2 agreement with Mitsubishi Heavy Industries worth Rs 1,387 crore combined (for high-value rotating and stationary airfoils), the Rolls-Royce seven-year defence engine contract, the Pratt & Whitney Canada agreement, and the Safran Aircraft Engines long-term understanding.

Management has noted that its wallet share across existing customers is only about 1 to 1.5%. The room to grow within relationships that are already established is substantial. As one analyst put it: the order book provides visibility, the wallet share provides runway.

Exports account for 90%+ of revenue. The company is overwhelmingly an export business, serving global OEMs from India.

The balance sheet carries moderate debt. Market cap is approximately Rs 10,000 crores. The stock trades at expensive valuations for any classical Ben Graham disciples. It listed in December 2023 and is still in its early public-market life.

Now here is the part where you need to go deep!

Azad is primarily an energy turbine blade company today. Aerospace, today is just 17% of revenue. The thesis that Azad is “solving the GTF crisis” requires understanding that: Azad manufactures the same class of hot-section components (blades, nozzles, combustor liners) that the GTF recall has created a global shortage of, and it has now signed contracts with four of the world’s major aero-engine OEMs. However, the bulk of its revenue (today) comes from power generation turbines, not jet engines. The aero-engine contracts are real, growing at 30%+ annually, and backed by multi-year agreements. The direction of travel is clear. But at 17% of revenue, aerospace is still the growth story, not the current reality.

Whether that growth story justifies the current multiples is a question I’ll leave to each reader.

The Capacity Expansion That Tells You Where This Is Going

Azad is building new manufacturing facilities that are approximately 10 times the scale of its current infrastructure. Phase 1 covers 94,899 square metres. Phase 2 covers 67,267 square metres. Combined, that is over 1.6 lakh square metres of new production space, compared to the existing 20,000 square metres across four units in Hyderabad.

Management has said these facilities will take 2 to 3 years to reach full utilisation. A new lean manufacturing facility dedicated specifically to Siemens has already been launched. The capex is being funded partly from IPO proceeds (the company raised capital in December 2023) and partly from operating cash flow.

This expansion is what the order book demands. You don’t sign a Rs 1,387 crore contract with Mitsubishi, a seven-year deal with Rolls-Royce, and long-term agreements with Pratt & Whitney Canada and Safran and then service them from just 20,000 square metres of space. The 10x facility expansion is the physical infrastructure required to convert a Rs 6,500 crore order book into revenue over the next five years.

How This Connects Back to the GTF Crisis

Let me tie the threads together, because the connection between an $8 billion engine recall and a turbine blade manufacturer in Hyderabad is real but requires careful articulation.

The GTF crisis created a surge in demand for hot-section engine components (turbine blades, nozzles, combustor liners, disc assemblies) that the existing global supply base cannot meet. Pratt & Whitney’s own MRO network is overwhelmed. Its suppliers are at capacity. The new forging press at Columbus won’t be online until 2028. Meanwhile, 835 aircraft sit on the ground and airlines are cannibalising nearly-new planes for parts.

At the same time, beyond the GTF recall, the broader aero-engine industry faces a structural supply-demand imbalance. The 17,000-aircraft backlog means new engines are needed at record rates. Ageing fleets require more MRO work. Safran’s aftermarket grew 30% in 2025. GE is spending $1 billion on supplier ramp-ups. Every major engine OEM is actively qualifying new suppliers in lower-cost geographies to add capacity.

Azad sits at the intersection of this demand. The company makes the exact category of components that are in global shortage: precision-forged and machined hot-section parts made from nickel superalloys, certified at zero-defect quality, for the same OEMs that build and maintain the world’s jet engines. Its energy turbine heritage gave it the technical capability. Its aero-engine contracts with Rolls-Royce, Pratt & Whitney Canada, Safran, and GE give it the certifications and customer access. The 10x facility expansion gives it the capacity roadmap.

Ofcourse, Azad is not going to single-handedly fix the GTF crisis. No single company will. But it is one of a very small number of qualified manufacturers globally that can produce the components the aero-engine MRO supply chain is desperate for. And it is scaling faster than almost any of them.

The Risks

As usual, none of my posts are a buy or sell recommendations. I read about interesting companies which I own (or are a part of my ever expanding watchlist) and write about them here in the public. The risks are worth knowing.

Valuation. At current multiples, the stock is priced for substantial growth that hasn’t materialised yet in the P&L. If aerospace contracts ramp slower than expected, or if the energy business faces cyclical weakness, the premium compresses sharply.

Aerospace is still small. 17% of revenue. The thesis depends on this growing to 30, 40, 50%+ over the next five years. Qualification cycles are long. Programme delays by OEMs are common. Growth can be lumpy. However, it must be noted that their other vertical runs as picks and shovels in the AI supercycle. So they are at the intersection of AI as well as Aerospace, getting them uniquely positioned at this intersection.

Execution on 10x expansion. Building facilities 10 times the current scale while maintaining zero-defect quality on superalloy components is a significant operational challenge. Any quality slip with an OEM like Rolls-Royce or Pratt & Whitney could be terminal for that relationship.

Customer concentration. A handful of global OEMs represent the bulk of the order book. Loss of a single major client would visibly impact the trajectory.

Competition. Bharat Forge has an established aerospace division making compressor blades and fan blades for Rolls-Royce. Godrej Aerospace supplies engine modules to Pratt & Whitney and GE. International competitors with deeper installed capabilities remain the primary competition.

What I Am Monitoring

Aerospace & Defence revenue as a percentage of total. Currently 17%. Movement toward 25%+ would confirm the shift from energy-dominant to a balanced portfolio. Track this quarterly.

Specific aero-engine programme ramp-ups. The Rolls-Royce defence contract, the P&W Canada agreement, and the Safran LTA are all in early stages. Revenue contribution from each becoming visible in quarterly disclosures would be a meaningful signal.

New facility utilisation. Phase 1 and Phase 2 expansion timelines. Management has guided 2-3 years to full utilisation. Early production milestones and customer qualifications at the new facilities are the tangible proof points. This (arguably), is the most important factor to monitor at this point of time.

EBITDA margins as aerospace scales. Current margins are around 39%. If aerospace carries higher margins than energy, the blended margin trajectory will tell you how valuable the mix shift is. Irrespective, as mentioned above, their O&G turbines business gives them enough runway. To top it up, Aerospace orderbooks are typically more long-tailed as compared to Power Infrastructure, and command a more stable margin.

Order book replenishment. Rs 6,500 crore provides strong visibility, but the market will want to see continued new contract wins, particularly in aerospace, to maintain the growth narrative beyond the current backlog.

Wallet share expansion. Management says current wallet share is 1 to 1.5% across customers. Movement to 3 to 5% with existing OEMs would validate the “land and expand” strategy without requiring new customer acquisition.

Tying It Together

When I wrote about Dynamatic, the thesis was about airframes: the world can’t build enough planes, and an Indian company earned its place in that supply chain through 17 years of patient execution. The thesis with Azad Engineering operates on the other side of the same aircraft. The world can’t repair its engines fast enough, the components in the engine’s hottest, most stressed section are the binding constraint, and a company that spent 15 years mastering superalloy blade manufacturing for power turbines is now applying that capability to the same components the aero-engine MRO network is desperate for.

The two stories are connected. The 17,000-aircraft backlog means more new engines are needed every year. The 835-aircraft grounding means existing engines need more replacement components than the supply chain can produce. Both create sustained, multi-year demand for precision-manufactured hot-section parts. Both are pulling Indian suppliers deeper into global programmes. And both reward companies that built their capabilities over time rather than trying to shortcut the qualification process.

Azad’s Rs 6,500 crore order book, its contracts with four of the world’s six major aero-engine OEMs, its 3.09 million units at zero PPM defects, and its 10x facility expansion all point in the same direction. Whether the stock at current multiples adequately prices the execution risk of scaling a business that is still 83% energy turbines is the central investment question. The industry tailwind is structural. The customer relationships are verified. The order book is real. What remains is the transition from a very good energy turbine component company that does some aerospace work to a global aerospace-and-energy platform where the aero-engine business becomes the growth engine.

That transition will play out over the next three to five years. The Phase 1 facility ramp and the first meaningful revenue from the Rolls-Royce and P&W Canada contracts will be the proof points. The numbers will tell the rest.

Disclaimer: This is for educational purposes only, and not investment advice. The author may or may not hold positions in the companies discussed. Do your own research and consult a financial advisor before making investment decisions.

Fantastic read. Loved how you connected a small technical issue to a global opportunity and highlighted Azad’s positioning without overhyping it.

Great read !! It’s benefitting the most from turbine/engine super cycle globally coz of both AI infrastructure n aerospace backlogs.